FINANCIAL-ACCOUNTING-AND-REPORTING Online Practice Questions and Answers

Questions 4

On December 2, 20X1, Flint Corp.'s board of directors voted to discontinue operations of its frozen food division and to sell the division's assets on the open market as soon as possible. The division reported net operating losses of $20,000 in December and $30,000 in January. On February 26, 20X2, sale of the division's assets resulted in a gain of $90,000. Assuming that the frozen foods division qualifies as a component of the business and ignoring income taxes, what amount of gain/loss from discontinued operations should Flint recognize in its income statement for 20X2?

A. $0

B. $40,000

C. $60,000

D. $90,000

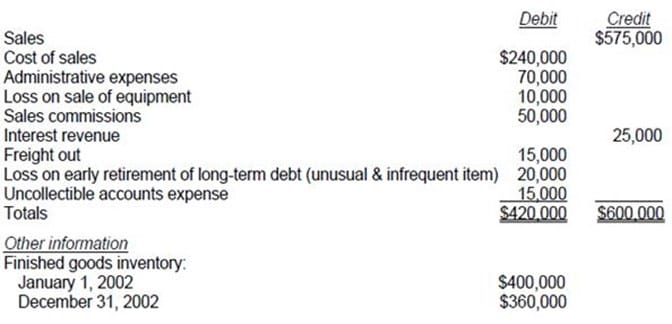

Questions 5

The following question is based on the following:

Vane Co.'s trial balance of income statement accounts for the year ended December 31, 2002, included

the following:

Vane's income tax rate is 30%.

In Vane's 2002 multiple-step income statement, what amount should Vane report as income from

continuing operations?

A. $126,000

B. $129,500

C. $140,000

D. $147,000

Questions 6

On November 1, 20X2, Smith Co. contracted to dispose of an industry segment. Throughout 20X2 the segment had operating losses. These losses were expected to continue until the segment's disposition. If a loss is projected on final disposition, how much of the operating losses should be included in the loss from discontinued operations reported in Smith's 20X2 income statement?

I. Operating losses for the period January 1 to October 31, 20X2.

II. Operating losses for the period November 1 to December 31, 20X2.

III.

Estimated operating losses for the period January 1 to February 28, 20X3.

A.

II only.

B.

II and III only.

C.

I and III only.

D.

I and II only.

Questions 7

If a company is not presenting comparative financial statements, the correction of an error in the financial statements of a prior period should be reported, net of applicable income taxes, in the current:

A. Retained earnings statement after net income but before dividends.

B. Retained earnings statement as an adjustment of the opening balance.

C. Income statement after income from continuing operations and before extraordinary items.

D. Income statement after income from continuing operations and after extraordinary items.

Questions 8

Rock Co.'s financial statements had the following balances at December 31:

What amount should Rock report as comprehensive income for the year ended December 31?

A. $400,000

B. $420,000

C. $520,000

D. $570,000

Questions 9

APB Opinion No. 28, Interim Financial Reporting, concluded that interim financial reporting should be viewed primarily in which of the following ways?

A. As useful only if activity is spread evenly throughout the year.

B. As if the interim period were an annual accounting period.

C. As reporting for an integral part of an annual period.

D. As reporting under a comprehensive basis of accounting other than GAAP.

Questions 10

Opto Co. is a publicly-traded, consolidated enterprise reporting segment information. Which of the

following items is a required enterprise-wide disclosure regarding external customers?

A. The fact that transactions with a particular external customer constitute more than 10% of the total enterprise revenues.

B. The identity of any external customer providing 10% or more of a particular operating segment's revenue.

C. The identity of any external customer considered to be "major" by management.

D. Information on major customers is not required in segment reporting.

Questions 11

The following items were among those that were reported on Lee Co.'s income statement for the year ended December 31, 1989:

The office space is used equally by Lee's sales and accounting departments. What amount of the abovelisted items should be classified as general and administrative expenses in Lee's multiple-step income statement?

A. $290,000

B. $325,000

C. $410,000

D. $500,000

Questions 12

During 1990, Fuqua Steel Co. had the following unusual financial events occur:

•

Bonds payable were retired five years before their scheduled maturity, resulting in a $260,000 gain. Fuqua has frequently retired bonds early when interest rates declined significantly.

•

A steel forming segment suffered $255,000 in losses due to hurricane damage. This was the fourth similar loss sustained in a 5-year period at that location.

•

A component of Fuqua's operations, steel transportation, was sold at a net loss of $350,000.

This was Fuqua's first divestiture of one of its operating segments.

Before income taxes, what amount of gain (loss) should be reported separately as a component of income

from continuing operations in 1990?

A. $260,000

B. $5,000

C. $(255,000)

D. $(350,000)

Questions 13

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with

Quo's president and outside accountants, made changes in accounting policies, corrected several errors

dating from 1992 and before, and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List B represents the general accounting treatment

required for these transactions. These treatments are:

•

Cumulative effect approach - Include the cumulative effect of the adjustment resulting from the accounting change or error correction in the 1993 financial statements, and do not restate the 1992 financial statements.

•

Retroactive or retrospective restatement approach - Restate the 1992 financial statements and adjust 1992 beginning retained earnings if the error or change affects a period prior to 1992.

•

Prospective approach - Report 1993 and future financial statements on the new basis but do not restate 1992 financial statements.

During 1993, Quo increased its investment in Worth, Inc. from a 10% interest, purchased in 1992, to 30%, and acquired a seat on Worth's board of directors. As a result of its increased investment, Quo changed its method of accounting for investment in Worth, Inc. from the cost method to the equity method.

List B

A. Cumulative effect approach.

B. Retroactive or retrospective restatement approach.

C. Prospective approach.

![]()

![]()

Home | About Us | Contact Us | FAQ | Guarantee Policy | Privacy Policy

Any charges made through this site will appear as Global Simulators Limited. All trademarks are the property of their respective owners.

Copyright © 2004-2025 pass2lead.com, All Rights Reserved.