CPA-REGULATION Online Practice Questions and Answers

Questions 4

In which of the following situations may taxpayers file as married filing jointly?

A. Taxpayers who were married but lived apart during the year.

B. Taxpayers who were married but lived under a legal separation agreement at the end of the year.

C. Taxpayers who were divorced during the year.

D. Taxpayers who were legally separated but lived together for the entire year.

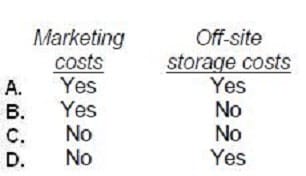

Questions 5

Under the uniform capitalization rules applicable to property acquired for resale, which of the following costs should be capitalized with respect to inventory if no exceptions are met?

A. Option A

B. Option B

C. Option C

D. Option D

Questions 6

During 1993 Kay received interest income as follows:

On U.S. Treasury certificates $4,000 On refund of 1991 federal income tax 500

The total amount of interest subject to tax in Kay's 1993 tax return is:

A. $4,500

B. $4,000

C. $500

D. $0

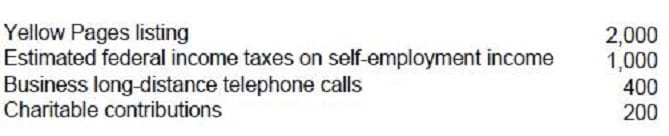

Questions 7

Rich is a cash basis self-employed air-conditioning repairman with 1993 gross business receipts of $20,000. Rich's cash disbursements were as follows:

What amount should Rich report as net self-employment income?

A. $15,100

B. $14,900 C. $14,100

D. $13,900

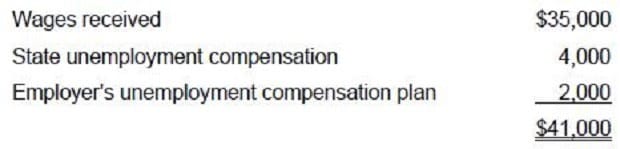

Questions 8

Porter was unemployed for part of the year. Porter received $35,000 of wages, $4,000 from a state unemployment compensation plan, and $2,000 from his former employer's company-paid supplemental unemployment benefit plan. What is the amount of Porter's gross income?

A. $35,000

B. $37,000

C. $39,000

D. $41,000

Questions 9

Don Wolf became a general partner in Gata Associates on January 1, 1989, with a 5% interest in Gata's profits, losses, and capital. Gata is a distributor of auto parts. Wolf does not materially participate in the partnership business. For the year ended December 31, 1989, Gata had an operating loss of $100,000. In addition, Gata earned interest of $20,000 on a temporary investment. Gata has kept the principal temporarily invested while awaiting delivery of equipment that is presently on order. The principal will be used to pay for this equipment. Wolf's passive loss for 1989 is:

A. $0

B. $4,000

C. $5,000

D. $6,000

Questions 10

A cash basis taxpayer should report gross income:

A. Only for the year in which income is actually received in cash.

B. Only for the year in which income is actually received whether in cash or in property.

C. For the year in which income is either actually or constructively received in cash only.

D. For the year in which income is either actually or constructively received, whether in cash or in property.

Questions 11

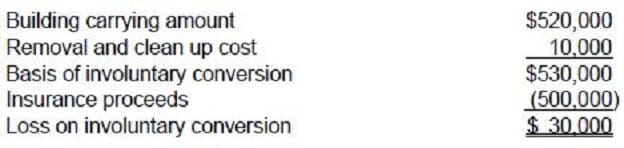

On December 31, 1989, a building owned by Pine Corp. was totally destroyed by fire. The building had fire insurance coverage up to $500,000. Other pertinent information as of December 31, 1989 follows:

During January 1990, before the 1989 financial statements were issued, Pine received insurance proceeds of $500,000. On what amount should Pine base the determination of its loss on involuntary conversion?

A. $520,000

B. $530,000

C. $550,000

D. $560,000

Questions 12

Ryan, age 57, is single with no dependents. On July 1, 1997, Ryan's principal residence was sold for the net amount of $500,000 after all selling expenses. Ryan bought the house in 1963 and occupied it until sold. On the date of sale, the house had a basis of $180,000. Ryan does not intend to buy another residence. What is the maximum exclusion of gain on sale of the residence that may be claimed in Ryan's 1997 income tax return?

A. $320,000

B. $250,000

C. $125,000

D. $0

Questions 13

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent. Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040. The Moores received $8,400 in gross receipts from their rental property during 1994. The expenses for the residential rental property were:

A. $0

B. $500

C. $900

D. $1,000

E. $1,250

F. $1,300

G. $1,500

H. $2,000

I. $2,500

J. $3,000

K. $10,000

L. $25,000

M. $50,000

N. $55,000

O. $75,000

![]()

![]()

Home | About Us | Contact Us | FAQ | Guarantee Policy | Privacy Policy

Any charges made through this site will appear as Global Simulators Limited. All trademarks are the property of their respective owners.

Copyright © 2004-2025 pass2lead.com, All Rights Reserved.